Welcome to State of the Market, our monthly roundup of key property market updates, with actionable insights for small and medium-sized property developers.

Key takeaways:

- House prices pause – affordability remains key constraint

- Rate outlook stabilises – lending conditions become clearer

- Planning-ready sites command a premium – developers prioritise certainty

- Construction activity remains subdued – cost pressures persist

- Funding structures matter more – flexibility creates advantage

1. House prices pause – affordability remains the key constraint

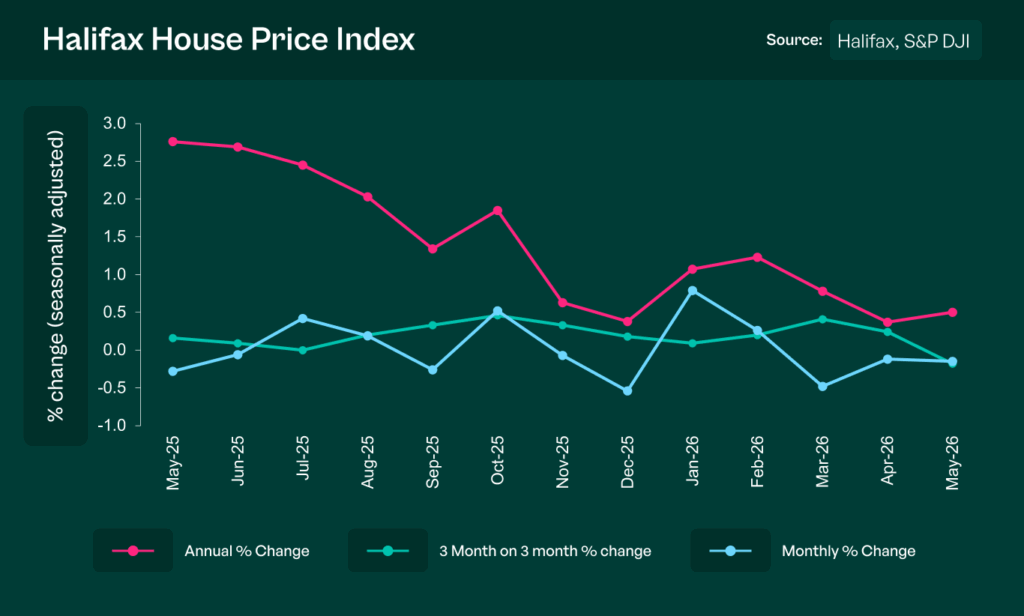

The housing market was fairly stable through May, with Halifax reporting only marginal movement in average house prices and annual growth continuing to slow. While pricing has held up better than many expected, affordability remains the defining constraint on market activity.

Higher mortgage costs relative to recent years continue to limit buyer purchasing power, particularly in less affordable regions. Demand remains present, but buyers are increasingly selective and focused on value, energy efficiency and realistic pricing.

Amanda Bryden, Head of Mortgages, Halifax, said:

Average house prices remained broadly stable in May, with a slight fall of -0.1% matching that seen in April. The typical property now costs £298,806, while the pace of annual growth edged up slightly to +0.5%. Property price trends continue to reflect the uncertainty linked to developments in the Middle East. Despite recent cuts to mortgage rates, higher inflation expectations have kept borrowing costs above the level seen at the start of the year, continuing to stretch affordability for many buyers and temper demand.

Source: Halifax House Price Index

What this means for SME developers:

The market continues to reward well-positioned schemes, but pricing discipline remains critical. Developers should focus on delivering products that align with local affordability rather than relying on broader house price inflation to support viability.

2. Rate outlook stabilises – lending conditions become clearer

The Bank of England held the base rate at 3.75% in June, marking its fourth consecutive decision to leave rates unchanged. While expectations for future rate cuts continue to fluctuate, the prolonged period of stability is helping borrowers, lenders and developers operate with greater confidence.

Mortgage pricing remains competitive, with some lenders continuing to reduce rates selectively as swap rate volatility eases. Although affordability remains a constraint for many buyers, the market is benefiting from a clearer interest rate environment than earlier in the year, when geopolitical tensions and inflation concerns drove significant uncertainty.

Source: Bank of England

What this means for SME developers:

While rates remain elevated compared with recent years, greater stability is improving visibility for both developers and buyers. Schemes with realistic pricing and clear exit strategies should benefit from a more predictable lending environment as the year progresses.

3. Planning-ready sites command a premium – developers prioritise certainty

Developers are becoming increasingly selective in their land acquisition strategies, prioritising sites with planning consent or a clear pathway to delivery. According to Savills, housebuilders are actively seeking to reduce risk by focusing on oven-ready opportunities and locations with stronger housing market fundamentals.

This reflects a wider shift towards certainty. With planning delays, build cost pressure and ongoing market uncertainty continuing to affect viability, developers are placing greater value on sites that can be progressed quickly and predictably.

Source: Market in Minutes: Residential Development Land – Savills

What this means for SME developers:

Well-consented sites are likely to remain in demand. Developers should carefully assess planning risk and recognise that certainty of delivery is increasingly influencing both land values and funding appetite.

4. Construction activity remains subdued – cost pressures persist

The latest RICS analysis suggests construction activity remains under pressure, with firms reporting weaker workloads alongside ongoing concerns around financing costs and project viability. While inflation has moderated significantly from recent peaks, elevated borrowing costs and continued cost pressures are still weighing on development activity.

The report highlights that access to credit and affordability challenges continue to influence decision-making across the sector, contributing to a more cautious operating environment despite improving stability elsewhere in the market.

Source: Construction activity weakens as credit and cost pressures persist – RICS

What this means for SME developers:

The challenge is no longer rapid cost inflation, but maintaining viability in a market where finance, affordability and delivery costs remain under pressure. Careful appraisal, realistic contingencies and disciplined project management remain essential.

5. Funding structures matter more – flexibility creates advantage

Competition within the debt market remains strong, but lenders are increasingly differentiating themselves through structure rather than simply pricing. According to Savills, borrowers are placing greater value on flexibility, certainty of execution and tailored funding solutions as market conditions remain uneven.

As development timelines, planning programmes and exit routes become more variable, the ability to structure finance around project-specific requirements is becoming increasingly important. This is creating opportunities for lenders that can offer flexibility, while reinforcing the importance of robust project planning and realistic funding assumptions.

Source: Debt market sees structure become as important as price – Savills

What this means for SME developers:

Access to funding is no longer just about securing the lowest rate. Developers should focus on finding finance structures that support project delivery, provide flexibility where needed and align with their exit strategy. In a more complex market, the right funding partner can be as valuable as the price of the debt itself.

Steve Deutsch, CrowdProperty CEO, comments:

The market is increasingly characterised by stability rather than significant change. House prices remain broadly flat, interest rate expectations have become clearer and developers are adapting to a more predictable operating environment. Planning certainty, disciplined site selection and robust project fundamentals are becoming increasingly important differentiators. Developers who focus on deliverability, realistic pricing and financial resilience remain well positioned to navigate the opportunities ahead.

And finally…

Here are five timely reads to keep you informed this month:

- UK economic and real estate briefing – BNP Paribas

- Rental growth slows as market becomes increasingly fragmented – BuyAssociation

- Small housebuilders squeezed by double-digit finance costs – REalyse

- Housing supply hits 10-year high as buyers enjoy more choice – The Intermediary

- Planning data update June 2026 – Savills

Together we build

At CrowdProperty, we work in close partnership with the developers we back – solving site, funding and delivery challenges together. Our team of property experts visits sites, shares insights, and helps developers stay ahead of the market.

We’ve funded over £900million in property projects, backed by 300+ years of combined property expertise. Our distinct ‘property finance by property people’ approach means we truly understand what developers need – and how to help them grow.

Learn more about our story and our team

Apply in just five minutes and get a Decision in Principle. Our property experts will then share their insights and initial funding terms, and work with you to find the right solutions to support the success of your project.

Explore projects we’ve already funded