Welcome to State of the Market, our monthly roundup of key property market updates, with actionable insights for small and medium-sized property developers.

Key takeaways:

- House prices recover slightly – affordability continues to cap growth

- Rate stability improves confidence – borrowing costs remain elevated

- Developers favour lower-risk sites – viability shapes land buying

- Construction slowdown eases – cost discipline remains critical

- Realistic appraisals becoming the market differentiator

1. House prices recover slightly – affordability continues to cap growth

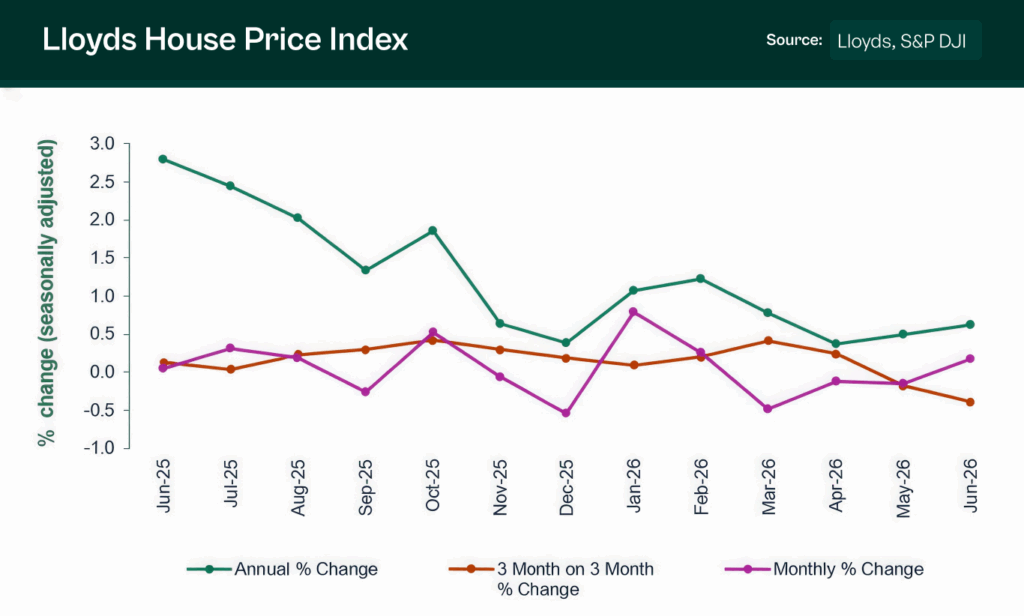

The latest Lloyds House Price Index reports a modest monthly increase in UK house prices, with prices rising by 0.2% in June following four consecutive months of little movement. The average UK property now stands at £299,330, while annual growth edged up to 0.6%.

Although the market has shown greater resilience than many expected, affordability continues to constrain buyer demand. Mortgage rates have eased from the highs seen earlier this year, providing some encouragement for buyers, but household budgets remain under pressure and demand continues to be highly selective.

Amanda Bryden, Head of Mortgages at Lloyds, said:

House prices rose for the first time in four months during June, increasing by +0.2%… While affordability remains stretched for many buyers, mortgage rates have eased from their recent highs, offering some encouragement to those considering a move… Looking ahead, we expect the housing market to continue moving at a measured pace. Lower borrowing costs should provide some support for demand, though affordability constraints remain an important factor.

Source: Lloyds House Price Index

What this means for SME developers:

The market continues to reward realistic pricing rather than optimism. While improving mortgage conditions should support buyer confidence over time, affordability remains the defining constraint on demand. Developers should continue to focus on schemes that align with local purchasing power and robust market fundamentals.

2. Rate stability improves confidence – borrowing costs remain elevated

The Bank of England has now held the base rate at 3.75% for several consecutive meetings, helping bring greater certainty to the lending environment. While expectations for future cuts continue to evolve, the prolonged period of stability has reduced volatility across mortgage markets.

Borrowers and lenders alike are benefiting from improved visibility, with mortgage pricing becoming more consistent than earlier this year. However, financing costs remain significantly higher than the ultra-low-rate environment developers became accustomed to during the previous decade.

Source: Bank of England

What this means for SME developers:

A more stable rate environment supports planning and forecasting, but higher borrowing costs remain a key consideration. Developers should continue to structure projects conservatively and ensure sufficient headroom within appraisals.

3. Developers favour lower-risk sites – viability shapes land buying

The UK development land market became more cautious in the second quarter, with weak sales rates and continued viability pressure weighing on demand. Savills reports that bidding remained comparatively resilient for schemes of around 75–200 homes, while appetite declined for larger sites carrying significant infrastructure requirements and longer delivery programmes.

Developers are continuing to prioritise sites with manageable scale, clearer planning routes and lower upfront exposure. Viability remains particularly challenging for brownfield and urban schemes, where higher build costs and delivery complexity continue to restrict activity.

Source: Market in Minutes: Residential Development Land – Savills

What this means for SME developers:

Lower-risk, deliverable sites remain the most attractive. Developers should scrutinise infrastructure obligations, planning complexity and programme length before acquisition, and avoid assuming that land values alone will compensate for difficult delivery conditions.

4. Construction slowdown eases – cost discipline remains critical

Recent BCIS industry surveys suggest the pace of contraction across construction is beginning to ease, but activity remains subdued and confidence continues to be affected by wider economic uncertainty. Industry professionals continue to identify build costs, labour availability and inflationary pressures as the biggest challenges facing delivery.

The ongoing conflict in the Middle East also continues to present upside risks to energy prices and material costs, reinforcing the need for careful procurement and cost management.

Source: The latest insight into construction activity (firm survey) – BCIS

What this means for SME developers:

While cost inflation has moderated, developers should avoid assuming construction costs have normalised. Robust contingencies, active procurement and realistic programmes remain essential to protecting margins.

5. Realistic appraisals becoming the market differentiator

One of the clearest trends emerging across the development finance market is the growing importance of disciplined appraisals. Developers are increasingly finding that assumptions around values, build costs and programme lengths are being scrutinised more rigorously during funding and valuation processes.

As viability margins tighten, successful schemes are those built on realistic forecasts, conservative assumptions and sufficient contingency. In the current market, careful underwriting is becoming as important as securing the right site.

Source: Construction Outlook: Poll of industry professionals – BCIS

What this means for SME developers:

Robust appraisals are becoming a competitive advantage. Developers who take a disciplined approach to values, costs and programme assumptions are more likely to secure funding and deliver profitable outcomes.

Steve Deutsch, CrowdProperty CEO, comments:

The market is continuing to stabilise, but success increasingly depends on disciplined execution rather than improving conditions alone. Affordability remains the defining influence on buyer demand, while developers are facing greater scrutiny around valuations, build costs and overall viability. The strongest opportunities remain available to those who plan conservatively, structure projects realistically and remain agile and make decisions based on realistic assumptions rather than optimistic forecasts.

And finally…

Here are five timely reads to keep you informed this month:

- Industry leaders call for Government action on housebuilding – The Intermediary

- Mayor unveils streamlined London plan with 558,000 home target – Property Week

- Judicial review reforms seek to accelerate construction projects – Construction News

- Construction output falls for second month – Construction Enquirer

- Glenigan construction review shows mixed figures across the industry – PBC Today

Together we build

At CrowdProperty, we work in close partnership with the developers we back – solving site, funding and delivery challenges together. Our team of property experts visits sites, shares insights, and helps developers stay ahead of the market.

We’ve funded over £900million in property projects, backed by 300+ years of combined property expertise. Our distinct ‘property finance by property people’ approach means we truly understand what developers need – and how to help them grow.

Learn more about our story and our team

Apply in just five minutes and get a Decision in Principle. Our property experts will then share their insights and initial funding terms, and work with you to find the right solutions to support the success of your project.

Explore projects we’ve already funded