Welcome to State of the Market, our monthly roundup of key property market updates, with actionable insights for small and medium-sized property developers.

Key takeaways:

- House prices dip – momentum slows amid rising uncertainty

- Mortgage repricing feeds through – buyer caution increases

- Build cost pressures persist – inflation risks building again

- Planning delays continue – programme risk remains elevated

- Refinance demand rising – proactive management important

1. House prices dip – momentum slows amid rising uncertainty

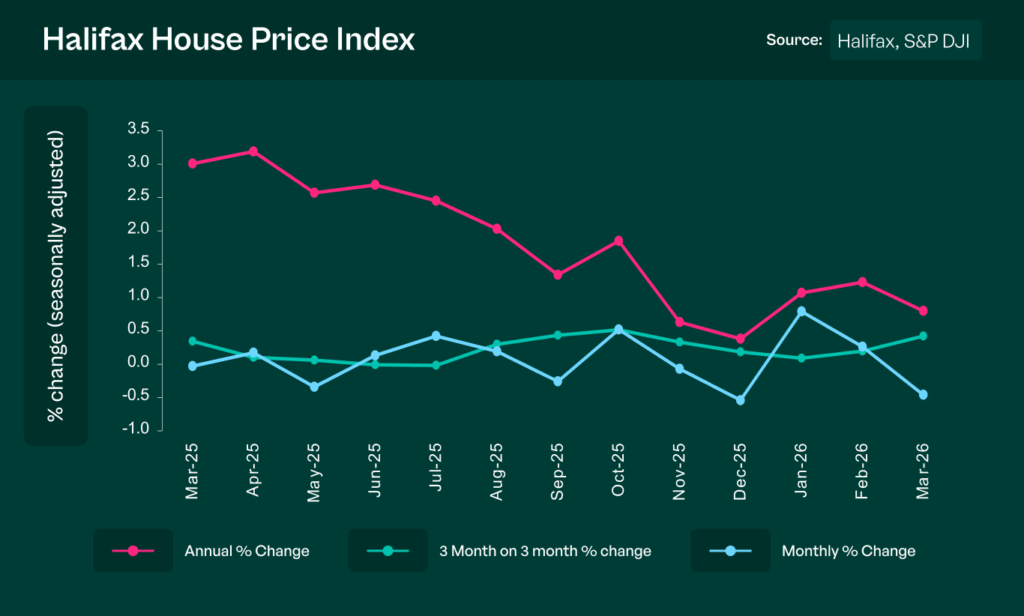

UK house prices fell slightly in March, reversing the modest gains seen earlier in the year. Halifax reports the average property price now stands at £299,677, with annual growth also easing as the housing market loses momentum following a stronger start to 2026.

The shift reflects growing uncertainty following the escalation of conflict in the Middle East. Rising energy prices have pushed up inflation expectations and mortgage rates, with lenders withdrawing cheaper products and repricing loans. This has weakened buyer confidence and reduced expectations of near-term interest rate cuts, dampening activity across the market.

Source: Halifax House Price Index

What this means for SME developers:

Demand remains, but is becoming more price-sensitive and cautious. Developers should prioritise realistic pricing, build in longer sales periods, and stress-test schemes against softer market conditions.

2. Mortgage repricing feeds through – buyer caution increases

Mortgage repricing following recent geopolitical developments is now feeding through more clearly into buyer behaviour. While the initial rate increases have been measured, the withdrawal of lower-cost products and reduced expectations for rate cuts have made buyers more cautious, particularly in higher-value segments.

This shift is beginning to affect transaction momentum, with longer decision-making timelines and increased sensitivity to pricing. Demand has not disappeared, but it is becoming more selective as affordability tightens.

Source: Mortgage cost warning – The independent

What this means for SME developers:

The impact of mortgage pricing is now being felt in the sales market. Developers should expect slower absorption rates and greater buyer sensitivity to pricing, particularly where affordability is stretched.

3. Build cost pressures persist – inflation risks building again

While construction cost inflation had begun to stabilise, recent geopolitical developments are reintroducing upward pressure. Rising energy costs and potential supply chain disruption linked to the Middle East conflict are likely to feed through into materials pricing and logistics costs.

At the same time, underlying cost pressures remain, with labour shortages and contractor pricing continuing to constrain margins. There is limited evidence of meaningful cost relief in the near term.

Source: Mounting cost pressures – Designing Buildings

What this means for SME developers:

Cost control remains critical. Developers should maintain robust contingencies and monitor input cost risks closely, particularly for energy-intensive materials and subcontractor pricing.

4. Planning delays continue – programme risk remains elevated

Planning delays remain a persistent challenge, with many local authorities continuing to operate under capacity constraints. Determination periods and the discharge of conditions are extending timelines, while delivery risks are compounded by contractor availability and build complexity.

These combined pressures continue to increase exposure to programme delays, extensions and refinancing risk across development projects. Despite ongoing policy discussions, meaningful improvement in planning timelines has yet to materialise.

Source: Planning uncertainty shaping development – Financial Reporter

What this means for SME developers:

Programme risk remains elevated. Developers should allow for extended timelines in appraisals and ensure funding structures are flexible enough to accommodate delays.

5. Refinance demand rising – proactive management important

As sales rates slow and development timelines extend, demand for refinancing solutions is increasing across the market. Developers are seeking extensions and refinancing options to manage longer exit periods and maintain project viability.

While this reflects a more measured sales environment rather than widespread distress, it highlights the importance of strong project fundamentals. Schemes with robust equity positions and clear exit strategies are better placed to secure support, while weaker projects may face greater pressure.

Source: Refinancing demand rises – The Intermediary

What this means for SME developers:

Early engagement with lenders is essential. Developers should plan refinancing scenarios in advance and maintain strong reporting and equity buffers to preserve flexibility.

Steve Deutsch, CrowdProperty CEO, comments:

The market is adjusting to renewed uncertainty. House prices have softened slightly and mortgage affordability has tightened, but underlying demand remains for the right product. Developers have navigated more challenging conditions in recent years, and those who maintain realistic pricing, strong equity and disciplined structuring are well placed to continue progressing schemes through 2026.

And finally…

Here are five timely reads to keep you informed this month:

- UK residential land market nearing a turning point – International Investment

- Taxing time for housebuilders – Property Week

- Resi construction levels 30% lower than 2025 – Development Finance Today

- Government’s housing target suffering from subsidence – The Guardian

- The Future Homes Standard – what this means for SME developers – CrowdProperty

Together we build

At CrowdProperty, we work in close partnership with the developers we back – solving site, funding and delivery challenges together. Our team of property experts visits sites, shares insights, and helps developers stay ahead of the market.

We’ve funded over £900million in property projects, backed by 300+ years of combined property expertise. Our distinct ‘property finance by property people’ approach means we truly understand what developers need – and how to help them grow.

Learn more about our story and our team

Apply in just five minutes and get a Decision in Principle. Our property experts will then share their insights and initial funding terms, and work with you to find the right solutions to support the success of your project.

Explore projects we’ve already funded