Welcome to State of the Market, our monthly roundup of key property market updates, with actionable insights for small and medium-sized property developers.

Key takeaways:

- House prices remain stable – but geopolitical risk clouds outlook

- Mortgage pricing volatility returns – lenders repricing loans

- Build cost inflation eases – but margins remain tight

- Residential planning applications rising – early pipeline recovery

- NPPF revisions proposed – sector warns ‘all bark and no bite’

1. House prices remain stable – but geopolitical risk clouds outlook

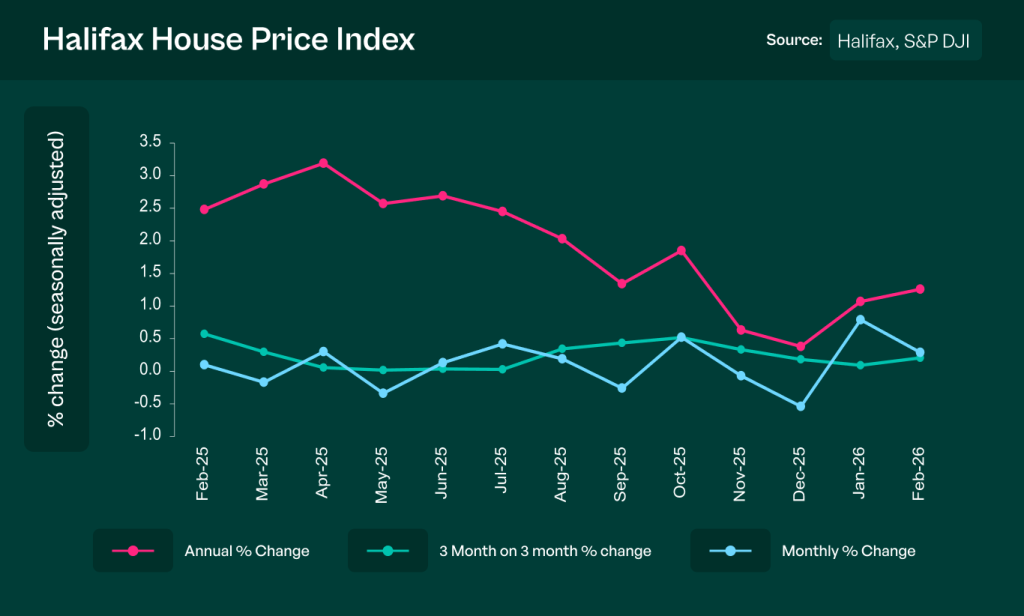

The UK housing market continued its steady start to 2026 through February. The latest Halifax House Price Index shows prices remained broadly stable, with modest annual growth and continued evidence of selective but resilient buyer demand. Well-priced homes in strong employment areas continue to transact, although affordability constraints still influence purchasing decisions.

However, market sentiment became more uncertain following the escalation of conflict involving Iran on 28 February. Rising oil prices and financial market volatility have already begun influencing inflation expectations and mortgage pricing, introducing a new macro risk for the housing market.

Source: Halifax House Price Index – February 2026

What this means for SME developers:

Buyer demand remains present for competitively priced homes, but macro volatility could slow improvements in affordability. Conservative GDV assumptions and flexible exit strategies remain prudent as markets adjust.

2. Mortgage pricing volatility returns – lenders repricing loans

Mortgage markets reacted quickly to the escalation in Middle East tensions, with rising oil prices pushing up inflation expectations and swap rates. Several lenders began repricing mortgage products in early March as markets adjusted to the potential for interest rates to remain higher for longer.

Mortgage pricing remains the single most important driver of housing market liquidity. Even small movements in mortgage rates can significantly affect buyer affordability and transaction volumes.

Source: Market shock pushes fixed rates towards imminent rise – Mortgage Soup

What this means for SME developers:

Mortgage pricing directly influencing exit liquidity. Developers should stress-test sales values and programme timelines against scenarios where mortgage affordability tightens again.

3. Build cost inflation eases – but margins remain tight

Construction cost inflation has slowed significantly compared with the spikes seen during 2022 and 2023. Materials availability has improved and price increases across several key categories have moderated, providing greater clarity for development appraisals.

Despite this improvement, build costs remain elevated relative to historic norms. Labour shortages and energy costs continue to influence contractor pricing and project viability.

Source: Building Materials and Components Statistics – GOV.UK

What this means for SME developers:

Improved cost visibility supports better feasibility planning, but disciplined procurement and contingency allowances remain essential to protect margins.

4. Residential planning applications rising – early pipeline recovery

Residential planning applications have begun to rise, suggesting early signs of activity returning to the development pipeline. Recent industry data indicates that more schemes are entering the planning system after a subdued period for new project starts, as developers reassess opportunities following stabilisation in house prices and construction costs.

While activity remains below long-term averages, the increase in applications points to cautious optimism across parts of the development sector. Developers appear to be progressing viable sites where planning risk is manageable and demand fundamentals remain strong.

Source: Residential planning applications on the rise – The Construction Index

What this means for SME developers:

The gradual return of planning activity suggests developers are beginning to move projects forward again. Sites with clear planning pathways and strong local demand may present opportunities as the pipeline begins to rebuild.

5. NPPF revisions proposed – sector warns ‘all bark and no bite’

The government’s proposed revisions to the National Planning Policy Framework (NPPF) have prompted widespread reaction across the property and construction sectors. Industry stakeholders are closely examining the potential impact of the proposed changes, which could affect housing delivery targets, planning policy interpretation and the viability of certain development sites.

Planning policy remains one of the most significant structural influences on development activity. Any adjustments to the NPPF have the potential to shape land supply, planning decisions and the speed at which housing schemes progress through the planning system.

Source: Sector reacts to draft revision to National Planning Policy Framework – New Civil Engineer

What this means for SME developers:

Changes to national planning policy can influence how local authorities assess development proposals. Developers should closely monitor emerging guidance and consider how revisions may affect site viability, housing delivery expectations and planning strategy.

Steve Deutsch, CrowdProperty CEO, comments:

February reinforces a market defined by discipline rather than exuberance. House prices remain broadly stable and we’re starting to see early signs of activity returning to the development pipeline, with planning applications picking up across parts of the sector. At the same time, proposed changes to national planning policy underline how important the planning environment remains for housing delivery. Developers who combine realistic pricing, strong equity and disciplined structuring remain best placed to navigate the market through 2026.

And finally…

Here are five timely reads to keep you informed this month:

- New public register to create ‘extra red tape’ – Property Industry Eye

- SME developers must be central to delivering regeneration – Housing Digital

- New Future Homes Standard campaign to help deliver low energy homes – PBC Today

- Construction activity decline continues – Builders Merchants News

- Planning performance statistics – GOV.UK

Together we build

At CrowdProperty, we work in close partnership with the developers we back – solving site, funding and delivery challenges together. Our team of property experts visits sites, shares insights, and helps developers stay ahead of the market.

We’ve funded over £900million in property projects, backed by 300+ years of combined property expertise. Our distinct ‘property finance by property people’ approach means we truly understand what developers need – and how to help them grow.

Learn more about our story and our team

Apply in just five minutes and get an instant Decision in Principle. Our property experts will then share their insights and initial funding terms, and work with you to find the right solutions to support the success of your project.

Explore projects we’ve already funded